Our Prediction About Bonds Was Right (And Our Pick Is Already Up 33%…)

We finally made it. After months of searching, planning, budgeting, and worrying, we finally made the big move this past weekend.

I’ve mentioned before that my wife and I made the decision to pull up our stakes and move out to the country. And not a minute too soon… available homes on the market are scarce, with prices soaring, and mortgage rates creeping up.

According to the Mortgage Bankers Association, the average 30-year mortgage rate is now 4.8%, shooting up by the most in a decade last week (and the highest since December 2018).

For the year so far, mortgage rates have climbed by nearly 1.5 percent. That’s the fastest advance since 1994.

While it’s true that mortgage rates remain relatively low by historical standards (remember the days of 12% mortgages in the ’80s, anyone?), one has to wonder how much the housing market (and homebuyers) can take from such a rapid advance.

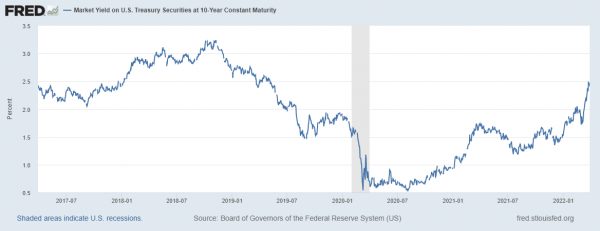

Remember, the conventional 30-year mortgage rate is correlated to the 10-year Treasury yield. Historically, you can expect a 30-year mortgage to trade about two percent (give or take) above the 10-year. So as the 10-year yield goes up, so do mortgage rates. And lately, bond market investors are not enamored with the 10-year, sending the yield well above 2% (remember, as the price goes down, yields go up, and vice versa).

Source: Federal Reserve Bank of St. Louis

The reason for the bond selloff is simple. Bond investors are positioning for more aggressive action from the Federal Reserve to rein in inflation, which is running at its hottest rate in 40 years. In fact, Fed Chair Jerome Powell recently commented that the central bank is prepared to act faster and potentially even raise rates by more than the usual 25 basis points at a time.

We Called It, Did You Profit?

If you remember, we made a prediction about the bond markets in 2022 as a part of our annual investment predictions report:

Interest rates will surge in 2022, slaughtering bonds, and devastating millions of unprepared income investors. If the bond market crashes, that’s bad news for everyone — even if you don’t own bonds. There are few escape routes from the bond debacle that the average investor is familiar with. But we’ve found a handful of obscure lifelines that could make 2022 the most lucrative year of your life.

I covered our central thesis in some detail in this article. And so far, our call to “short” Treasury Bonds has been spot on (meaning if bond prices fall, and yields go up, then you make money)…

In that article, I mentioned that there is a way for investors to “short” Treasury bonds without having to be a savvy Wall Street trader. In fact, we said there were two exchange-traded funds (ETFs) that we liked that do all the work for you.

You simply buy one of these funds, which give you short exposure to long-dated Treasuries, and profit.

But you have to remember that things are a little different in the world of bonds. A 1% move is a pretty big deal, for example. So in our usual fashion of “bold” predictions that are a little outside of the box, both of our ETF recommendations were leveraged, which means they will move more dramatically than the underlying market. So generally speaking, a 1% move in the markets should translate into a 2% or 3% move with these ETFs.

You can see how that’s worked out for investors who followed our recommendation. One of our recommendations, the Proshares UltraPro Short 20+ Year Treasury ETF (NYSE: TTT), is already up 33% this year (and has spiked as high as 42%)…

Remember, these leveraged short ETFs are typically designed for short-to-medium-term trades. And they do carry some risk. That said, there could still be plenty of life left in this trade if you want to take a flier.

In the meantime, go here to get more details on the rest of our predictions right now.